TL;DR:

- Account management risks extend beyond relationships to include operational, financial, security, and communication vulnerabilities that can quietly erode value. Professionals often underestimate these risks, mistakenly relying on good intent instead of structured processes and monitoring systems. Implementing scoring, automation, documentation, and proactive communication effectively mitigates these interconnected threats.

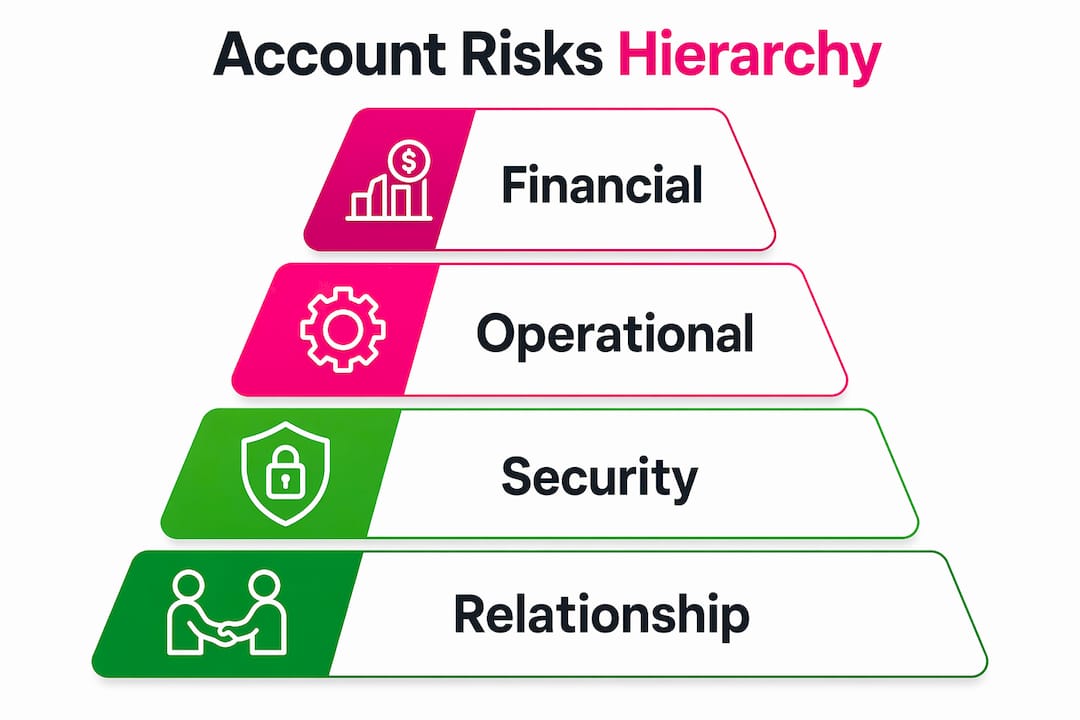

Most business professionals think account management is fundamentally about relationships. It is not. Understanding what are account management risks means recognizing that relationships are only one layer of a much more complex operational system. Beneath every client interaction sit financial exposures, security vulnerabilities, process failures, and communication breakdowns that can quietly erode revenue, damage trust, and destabilize entire portfolios. If you manage accounts without a structured view of these risks, you are already exposed.

Key takeaways

| Point | Details |

|---|---|

| Risks go beyond relationships | Account management challenges span operational, financial, security, and communication categories that most professionals underestimate. |

| Involuntary churn is a hidden threat | A significant share of account losses come from payment failures and process gaps, not client dissatisfaction. |

| Security threats are escalating fast | Credential stuffing and account takeovers cause direct financial losses and long-term trust damage across trading and business accounts. |

| Health scoring prevents late surprises | Monitoring account health with scoring systems enables early intervention before accounts reach a critical or lost state. |

| Automation reduces human error exposure | Replacing manual tracking with automated tools cuts workload, improves accuracy, and supports proactive risk management. |

What are account management risks in practice

Account management risks are the categories of threat that can damage, destabilize, or destroy the value of a client or trading account relationship. Most people define these risks too narrowly, focusing on whether a client is happy or whether calls are being returned. The reality is that account management operates as a structured operational system first and a relationship practice second.

There are four primary risk categories every account manager or trader should understand.

- Operational risks cover process failures, manual errors, churn from payment issues, and poor escalation handling.

- Financial risks include revenue leakage, unprofitable accounts, budget pressure from clients, and mismanaged scope.

- Security risks involve credential theft, account takeover fraud, and unauthorized trading activity.

- Relationship risks encompass stakeholder changes, competitive vulnerability, and poor communication during service failures.

Each category interacts with the others. A security breach creates a communication crisis. A payment failure becomes an operational failure when no recovery process exists. Understanding types of account risks as interconnected, not isolated, is the first shift serious professionals need to make.

Why professionals underestimate these risks

The biggest contributor to underestimating account management challenges is the assumption that good intent substitutes for good process. An account manager who genuinely cares about clients can still lose them through payment processing errors, credential exposure, or inconsistent follow-up. Caring is not a system. These risks require structured responses, not just good relationships.

Operational risks that erode account performance

Operational risks are the quiet killers in account management. They do not usually announce themselves with a dramatic client exit. They accumulate through small process failures until an account deteriorates past recovery.

Manual workflows are a primary culprit. 83% of Customer Success Managers still rely on spreadsheets for account tracking, and 45% cite workload as the primary cause of burnout. When account data lives in a spreadsheet that one person maintains, errors multiply. Updates get missed. At-risk signals get ignored because no one is looking at the right data at the right time.

Involuntary churn is a specific operational risk that deserves its own attention. 20 to 40% of SaaS churn is involuntary, meaning it comes from payment failures like expired cards or failed transactions rather than client dissatisfaction. The client never intended to leave. The process simply failed to catch and resolve the issue before the account lapsed.

Multi-account abuse adds another layer of operational complexity. 7.4% of AI company sign-ups involve multi-account abuse costing $35 per $100 disputed. For traders managing multiple accounts, understanding multi-account risk management is not optional. It is a core operational discipline.

The following common account management issues compound operational exposure:

- No structured escalation path when accounts show distress signals

- Lack of account health scoring or monitoring cadence

- Reactive rather than proactive client outreach

- No formal recovery plan when a payment failure or service gap occurs

Pro Tip: Build a tiered account health score from day one. Track engagement frequency, payment status, and product usage together. A score that falls below a defined threshold should trigger automatic escalation, not a manual reminder to someone who may already be overwhelmed.

Resolving hard payment declines requires particular care. Hard declines risk issuer fraud blocks if retried automatically. Manual outreach to request updated payment details is the only reliable resolution path, and most teams have no documented process for it.

Financial risks tied to client portfolios

Financial risks in account management are often camouflaged as relationship problems. A client who constantly pushes back on fees, requests scope expansions without additional budget, or pays late is not just a difficult relationship. They are a financial liability with a specific cost profile.

Revenue leakage is one of the most common accounting risk factors in agency and advisory work. It occurs when teams deliver more than what is contracted, absorb costs from scope creep, or fail to bill for incremental work. The client relationship may feel stable, but the profitability is eroding with every unbilled hour.

Here is a direct comparison of how profitable versus unprofitable accounts typically differ across key dimensions:

| Factor | Profitable account | Unprofitable account |

|---|---|---|

| Scope behavior | Respects contracted scope | Regularly requests out-of-scope work |

| Payment behavior | Pays on time, minimal disputes | Late payments, frequent chargebacks |

| Engagement quality | Strategic conversations | Tactical micromanagement |

| Response to value | Attributes outcomes to your work | Attributes outcomes to other factors |

| Retention signal | Renews or expands proactively | Renews only under pressure or discounts |

The key financial risks in client management include:

- Accepting scope expansions without commercial conversations

- Retaining accounts purely for revenue volume when margin is negative

- Allowing clients to dictate pricing under competitive threat without a structured response

- Failing to track account-level profitability, not just total portfolio revenue

Deciding to exit an unprofitable client relationship is one of the harder decisions in account management, but it is sometimes the right financial one. Holding onto accounts that consistently cost more to serve than they generate in revenue pulls resources away from profitable relationships.

Security and fraud risks in account management

Security risks are where account management challenges intersect most directly with financial catastrophe. For traders and financial account managers especially, a single breach can be irreversible.

Credential stuffing attacks on consumer login endpoints grew 148% year-over-year, with an average direct fraud loss of $12,000 per confirmed account takeover incident. The attack method is straightforward and scalable. Fraudsters acquire large databases of leaked username and password combinations, then run automated scripts against login endpoints until valid credentials produce access. The compromised account then becomes the vehicle for fraud.

In trading specifically, the threat goes further. Fraudsters use imposter websites and stolen credentials to access investment accounts, execute unauthorized trades, and coordinate pump-and-dump schemes. This is not a theoretical risk. It is an active threat environment that financial regulators have formally warned about.

| Security risk type | How it happens | Potential impact |

|---|---|---|

| Credential stuffing | Automated login attempts using leaked passwords | Account takeover, unauthorized trades |

| Phishing and impersonation | Fake websites or contacts impersonating known parties | Stolen credentials, fraudulent instructions |

| Insider access misuse | Former employees or shared login credentials | Data exposure, unauthorized account changes |

| Weak authentication | No multi-factor authentication on account access | Fast, undetected account compromise |

Pro Tip: Treat any login from a new device or unfamiliar IP address as a potential threat. Set up real-time alerts for unusual login activity and establish a documented response protocol so your team knows exactly what to do in the first 60 minutes after a suspected breach.

The SEC’s guidance on RIA compliance red flags also highlights identity theft vulnerabilities as a category requiring active mitigation, not just awareness. For anyone managing financial accounts professionally, the compliance and fraud prevention elements of security are inseparable.

Trade copier security practices like strong password protocols, multi-factor authentication, and running operations on a dedicated VPS reduce the attack surface significantly. The principle is simple: minimize shared access, eliminate weak credentials, and monitor for anomalies.

Relationship and communication risks

Relationship risks are real, but they are often misdiagnosed. The actual risk is not that a client dislikes you. It is that a structural communication gap, a stakeholder departure, or a competitive approach reveals that your value proposition was never clearly established.

When a primary client contact leaves, the relationship risk becomes existential if that person was your only meaningful connection within the account. The new stakeholder has no loyalty to you, no history of your work, and no reason not to evaluate alternatives. Effective account managers build relationships at multiple levels within client organizations specifically to prevent this single-point-of-failure dynamic.

The risks in client management from poor communication compound quickly:

- Clients fill information gaps with negative assumptions when issues are not proactively disclosed

- Delays in acknowledging service failures signal incompetence rather than professionalism

- Competing on price when challenged by a competitor signals that your value is unclear

- Transactional communication patterns signal that you view the relationship as a contract, not a partnership

Prompt, solution-oriented communication within 2 to 4 hours of a service failure leads to significantly higher long-term client loyalty than accounts where nothing ever goes wrong. The counterintuitive reality is that a well-managed problem builds more trust than a smooth track record, because it demonstrates how you behave under pressure.

Competitive vulnerability is a separate but related risk. The strongest response to a competitive threat is not matching a competitor point-by-point on price or features. It is deepening the evidence of unique value you deliver that the competitor cannot replicate.

How to mitigate account management risks

Knowing the risk categories is only useful if you act on them. The following steps represent a practical framework for reducing exposure across all four risk types.

-

Implement account health scoring. Assign scores based on payment behavior, engagement frequency, product usage, and open support issues. Critical accounts with health scores below 50 require executive intervention within 24 to 48 hours. At-risk accounts with scores between 50 and 75 should receive recovery plans within 5 business days.

-

Automate what manual tracking misses. Automation reduces churn prediction errors and cuts the manual workload that leads to burnout and dropped signals. For traders managing multiple accounts, automation tools that handle lot sizing, risk scaling, and execution remove the human error layer from high-stakes decisions.

-

Document escalation and recovery protocols. Every account team should have a written protocol for payment failures, service gaps, and security incidents. Without documentation, response quality depends entirely on whoever is available at the moment.

-

Build security into your standard operating process. Multi-factor authentication, dedicated VPS environments for trading accounts, and access controls are not optional for professional account managers. Prop firm automation strategies are a useful reference for how systematic risk controls translate into operational stability.

-

Have commercial conversations early and regularly. Financial risks compound when scope, profitability, and account value are never discussed directly. Schedule quarterly reviews that include explicit conversations about ROI, budget, and strategic direction. Do not wait for a renewal conversation to discover that the relationship is at risk.

-

Diversify stakeholder relationships. Map key contacts within every significant account and identify gaps. If you have only one senior contact and that person leaves, you have a relationship risk you could have eliminated.

My take on account management risks

I have spent years watching account managers conflate relationship quality with account stability. They are not the same thing. I have seen genuinely warm, well-liked account managers lose major clients because no one had documented the escalation path, tracked the account health score, or had the commercial conversation that needed to happen six months earlier.

The shift I think matters most is recognizing that account management is an operational system, not a personality type. You can be the most personable person in the room and still expose your portfolio to avoidable risks by relying on intuition over process.

What I have learned from following this space closely is that the teams who manage risks well are not necessarily the ones with the deepest client relationships. They are the ones with the most reliable systems for detecting problems early, the clearest protocols for responding quickly, and the discipline to have uncomfortable commercial conversations before they become urgent ones.

Automation and analytics are not replacing good account managers. They are amplifying what good account managers can actually do. If you are still running your account portfolio from a spreadsheet in 2026, you are not just behind on tools. You are accepting unnecessary risk.

— Rimantas

Protect your trading accounts with Mt4copier

Managing accounts across multiple MetaTrader terminals compounds every risk category covered in this article. Each additional account is another surface for operational errors, unauthorized access, and manual execution mistakes. Mt4copier addresses the operational and security layer directly.

Local Trade Copier runs entirely on your local Windows machine or VPS with no cloud routing, no external server latency, and one IP address handling all trade replication. Your account data stays on your machine. For prop firm traders and independent account managers, that matters enormously from both a security and a compliance standpoint. The account security best practices built into Mt4copier’s VPS-based setup reduce your exposure to credential-based attacks and unauthorized access. Explore the full feature set and start a 7-day free trial to see how local execution changes your risk profile.

FAQ

What are the main types of account management risks?

The four primary types are operational risks (process failures, churn), financial risks (revenue leakage, unprofitable accounts), security risks (credential stuffing, account takeover), and relationship risks (stakeholder changes, poor communication). Each category can trigger losses in the others if left unmanaged.

How do you mitigate risks in client management?

Start with account health scoring to detect at-risk accounts early, document escalation protocols for payment and service failures, implement multi-factor authentication for all account access, and schedule regular commercial conversations to address financial exposure before it becomes a crisis.

What is involuntary churn and why does it matter?

Involuntary churn is account loss caused by payment failures rather than client dissatisfaction. It accounts for 20 to 40% of total churn in subscription businesses. Since the client did not choose to leave, a structured recovery process can recover a large share of these accounts if acted on quickly.

How does credential stuffing threaten account management?

Credential stuffing uses automated scripts to test stolen username and password combinations against login systems. Attacks on consumer login endpoints grew 148% year-over-year, and each confirmed account takeover causes an average direct loss of $12,000. Multi-factor authentication is the most effective single defense.

When should you exit an unprofitable client account?

Exit decisions are warranted when an account consistently generates negative margin after accounting for service delivery costs, payment disputes, and scope creep, and when multiple commercial conversations have failed to reestablish a sustainable financial basis for the relationship.

Recommended

- Why use account management in forex? Boost control

- Prop Firm Account Management Tips: Maximize Efficiency

- Mitigate forex trading risk for multi-account success